18.6. Hypothesis Testing and Confidence Intervals#

Recall that for single variable datasets, it was usually not enough to simply compute a statistic such as a sample mean. For instance, if looking at a sample from a larger population. The sample mean will hopefully be close to the population mean, it probably won’t be exactly the same. For this reason, we need to report not just the sample mean, but a confidence interval of plausible values for the population mean.

Similarly, when performing an A/B-test it is not enough to report a difference in means between group A and group B, we also need to compute a \(p\)-value that indicates the probability the difference in means arose by random chance.

As we will see these concept both have an analogues for regressions.

18.7. Simple Linear Regressions.#

It should be noted that the techniques we are about to use, will not always be statistically valid. There are a few things to check for before using the following techniques to test for significance or build a confidence interval for a linear regression. The most basic form of these assumptions is known as a “Linear Model with Equal Variance”.

18.8. Linear Model with Equal Variance#

A Linear Model with Equal Variance means that the population our data is being drawn from satisfies the following assumptions

If \(\mu_{Y|X}\) is the average value of \(Y\) among the subpopulation of values with \(x=X\), then

$\(\mu_{Y|X} = \alpha + \beta X\)$.

For instance if \(Y\) is sale price and \(X\) is square footage, then \(\mu_{Y,2200}\) would be the average sale price of all 2200 square foot homes. The first assumption says that there are numbers \(\alpha\) and \(\beta\), so that if we looked at all home sales, the average sale price of homes with square footage equal to \(X\) would be given exactly by \(\alpha+\beta X\) for any \(X\).

If \(\sigma_{Y|X}^2\) is the variance in \(Y\) in the subpopulation of values with \(x=X\), then \(\sigma_{Y|X}^2\) doesn’t depend on \(X\), that is there is some number \(\sigma\) so $\( \sigma_{Y|X}^2 = \sigma^2\)$.

For instance, if \(Y\) is sale price and \(X\) is square footage, then \(\mu_{Y,2200}\) would be the variance in sale price among all \(2200\) square foot homes. The second assumption says \(\mu_{Y,2200}=\mu_{Y,X}\) for any other value of \(X\).

18.9. Diagnostics for Linear Model with Equal Variance.#

We usually won’t know for sure if the population our data comes from satisfies the Linear Model with Equal Variance. We discuss here a few properties of a data set that can suggest either that the conditions are satisfied or that they are contradicted.

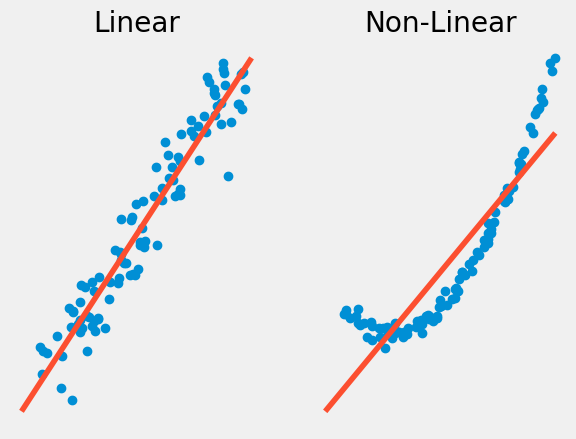

Linearity vs Non-linearity#

The first property our data must have is linearity, meaning that \(\mu_{Y|X}\) is a linear function of \(X\). Non-linearity occurs when the relationship between \(X\) and \(Y\) is not a linear one. In this case, you may want to use another type of regression such a logistic or polynomial regression. Something we will talk about in a further chapter.

Show code cell source

# generate homoskedastic data.

s_size = 100

a=-3

b=10

np.random.seed(346)

x_homsc = np.random.uniform(a,b,size=s_size)

y_homsc = x_homsc + np.random.normal(2,1,size=s_size)

p_hom = np.poly1d(np.polyfit(x_homsc,y_homsc,1))

fig, axs = plt.subplots(1, 2);

axs[0].plot(x_homsc, y_homsc, "o");

axs[0].plot(np.arange(a-1,b+1), p_hom(np.arange(a-1,b+1)), "-");

axs[0].set_title('Linear');

axs[0].axis('off');

# generate heteroskedastic data

x_het = np.random.uniform(a,b,size=s_size)

y_het = (x_het**2) + np.random.normal(0,2,size=s_size)

p_het = np.poly1d(np.polyfit(x_het,y_het,1))

axs[1].plot(x_het, y_het, "o");

axs[1].plot(np.arange(a-1,b+1), p_het(np.arange(a-1,b+1)), "-");

axs[1].set_title('Non-Linear');

axs[1].axis('off');

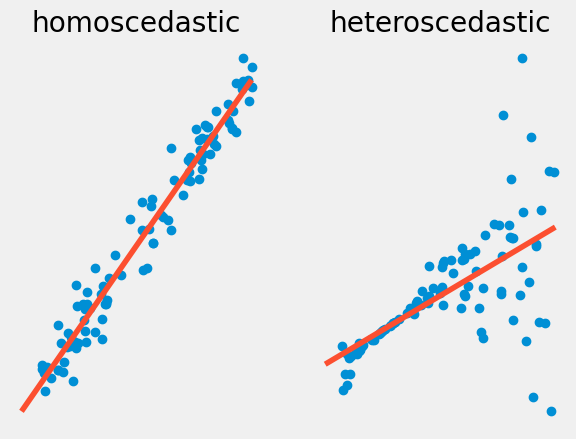

Homoscedasticity vs. Heteroscedasticity#

The second property our data must have is homoscedasticity, this means that the residuals of \(y\) around the regression line stay the same as \(x\) varies. Data that does not have this feature is heteroscedastic, while a lot of data sets have some heteroscedasticity, and a little bit might be acceptable, too much will harm the validity of the statistical analysis.

We can see examples of both types of behavior in the graphs below of a simulated data set. Note for the homoscedastic data, the residuals of \(y\) around \(x\) stay mostly the same. For heteroscedadstic data, for large \(x\) values the \(y\) values start to vary wildly around the regression line.

In terms of the model this means that the variance \(\sigma_{Y|X}^2\) varies as \(X\) changes.

Show code cell source

# generate homoskedastic data.

s_size = 100

a=-3

b=10

np.random.seed(344)

x_homsc = np.random.uniform(a,b,size=s_size)

y_homsc = x_homsc*0.5 + np.random.normal(5,0.5,size=s_size)

p_hom = np.poly1d(np.polyfit(x_homsc,y_homsc,1))

fig, axs = plt.subplots(1, 2);

axs[0].plot(x_homsc, y_homsc, "o");

axs[0].plot(np.arange(a-1,b+1), p_hom(np.arange(a-1,b+1)), "-");

axs[0].set_title('homoscedastic');

axs[0].axis('off');

# generate heteroskedastic data

x_het = np.random.uniform(a,b,size=s_size)

y_het = x_het*4 + 5 + (x_het**2)*np.random.normal(0,0.5,size=s_size)

p_het = np.poly1d(np.polyfit(x_het,y_het,1))

axs[1].plot(x_het, y_het, "o");

axs[1].plot(np.arange(a-1,b+1), p_het(np.arange(a-1,b+1)), "-");

axs[1].set_title('heteroscedastic');

axs[1].axis('off');

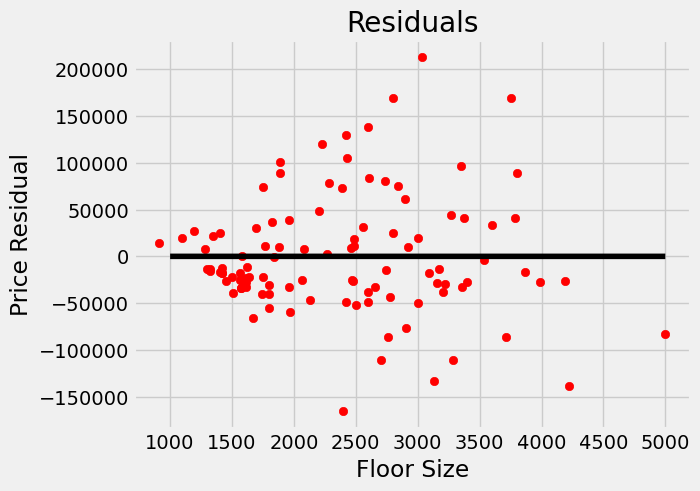

18.10. Residuals#

A quick way to get a sense of potential heteroscedasticity in your data, is to look at the graph of residuals. Recall that for our regression function \(f(x)\) the \(i\)-th residual is given by $\(\epsilon_i = y_i-f(x_i).\)$

We can graph the residuals for our housing data, and notice some heteroscedasticity, namely the variance seems to increase as square footage increases.

lin_regress = ols(housing_df['floor_size'],housing_df['sold_price'])

residuals = housing_df['sold_price']-(housing_df['floor_size']*lin_regress[0]+lin_regress[1])

plt.scatter(housing_df['floor_size'],residuals,color="red")

plt.xlabel("Floor Size")

plt.ylabel("Price Residual")

plt.title("Residuals")

plt.plot(np.arange(1000,5000), (np.arange(1000,5000))*0, "-",color="black");

plt.show()

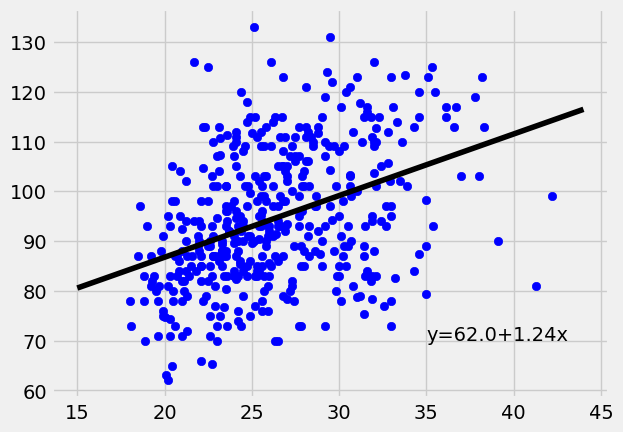

Diabetes Data Set#

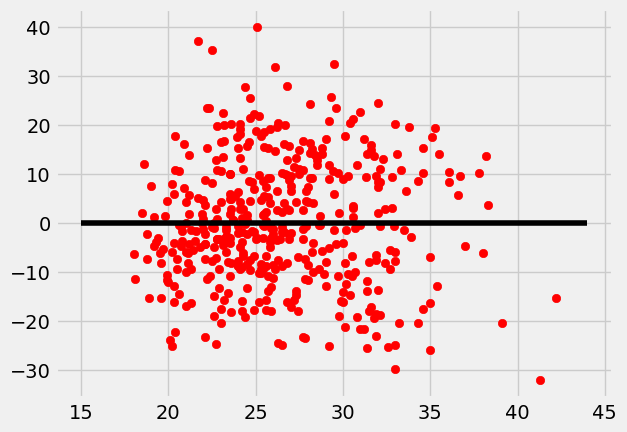

Since our first data set suffered from some heteroscedasticity. Let’s take a look at another. This diabetes data set comes from https://www4.stat.ncsu.edu/~boos/var.select/diabetes.html. It is a collection of health data from 442 diabetes patients. Looking at the residuals we see the data looks homoscedastic.

diabetes = pd.read_csv("diabetes.tsv",delimiter="\t")

diabetes

| AGE | SEX | BMI | BP | S1 | S2 | S3 | S4 | S5 | S6 | Y | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 59 | 2 | 32.1 | 101.00 | 157 | 93.2 | 38.0 | 4.00 | 4.8598 | 87 | 151 |

| 1 | 48 | 1 | 21.6 | 87.00 | 183 | 103.2 | 70.0 | 3.00 | 3.8918 | 69 | 75 |

| 2 | 72 | 2 | 30.5 | 93.00 | 156 | 93.6 | 41.0 | 4.00 | 4.6728 | 85 | 141 |

| 3 | 24 | 1 | 25.3 | 84.00 | 198 | 131.4 | 40.0 | 5.00 | 4.8903 | 89 | 206 |

| 4 | 50 | 1 | 23.0 | 101.00 | 192 | 125.4 | 52.0 | 4.00 | 4.2905 | 80 | 135 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 437 | 60 | 2 | 28.2 | 112.00 | 185 | 113.8 | 42.0 | 4.00 | 4.9836 | 93 | 178 |

| 438 | 47 | 2 | 24.9 | 75.00 | 225 | 166.0 | 42.0 | 5.00 | 4.4427 | 102 | 104 |

| 439 | 60 | 2 | 24.9 | 99.67 | 162 | 106.6 | 43.0 | 3.77 | 4.1271 | 95 | 132 |

| 440 | 36 | 1 | 30.0 | 95.00 | 201 | 125.2 | 42.0 | 4.79 | 5.1299 | 85 | 220 |

| 441 | 36 | 1 | 19.6 | 71.00 | 250 | 133.2 | 97.0 | 3.00 | 4.5951 | 92 | 57 |

442 rows × 11 columns

Show code cell source

x = diabetes["BMI"]

y = diabetes["BP"]

lin_regress = ols(x,y)

plt.scatter(x,y,color="blue")

plt.plot(np.arange(15,45), lin_regress[0]*np.arange(15,45)+lin_regress[1], "-",color="black");

plt.text(x=35,y=70,s="y="+str(round(lin_regress[1],2))+"+"+str(round(lin_regress[0],2))+"x")

plt.show()

x = diabetes["BMI"]

y = diabetes["BP"]

lin_regress = ols(x,y)

residuals = y-(x*lin_regress[0]+lin_regress[1])

plt.scatter(x,residuals,color="red")

plt.plot(np.arange(15,45), np.arange(15,45)*0, "-",color="black");

plt.show()

18.11. Hypothesis Testing for Linear Regression.#

Hypothesis Testing for Linear Regression, is a way to measure if there is a relationship between \(X\) and \(Y\) at all. Our hypothesis for a two sided-test would be as follows.

If we assume we have a Linear Model with Equal Variance, with \(\mu_{Y|X} = \alpha+\beta X\) then these hypothesis can be stated as follows

Of course these could be modified to allow for one sided hypothesis testing as well.

If there is no relationship between \(X\) and \(Y\), then any observed relationship is a result of random chance. In this scenario permuting the \(Y\)-values would give us a new dataset that was just as likely as our observed data set. Repeating this process and compute the slope of the observed regression lines gives us a distribution of slopes under the null hypothesis. We compare this distribution to our initial observed slope to compute a \(p\)-value.

The code below computes the \(p\)-value for the diabetes dataset.

sample_slope = ols(diabetes["BMI"],diabetes["BP"])[0]

null_slopes=[]

for i in range(1000):

# single bootstrap resample

shuffled_bp = np.random.choice(diabetes["BP"],len(diabetes["BP"]),replace=False)

# compute bootstrap statistic

shuffled_slope = ols(boot["BMI"],shuffled_bp)[0]

#store bootstrap statistic - sample statistic

null_slopes.append(shuffled_slope)

#compute $p$-value for two sided test

(sum(np.abs(np.array(null_slopes)) >= np.abs(sample_slope)))/1000

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

Cell In[9], line 8

6 shuffled_bp = np.random.choice(diabetes["BP"],len(diabetes["BP"]),replace=False)

7 # compute bootstrap statistic

----> 8 shuffled_slope = ols(boot["BMI"],shuffled_bp)[0]

9 #store bootstrap statistic - sample statistic

10 null_slopes.append(shuffled_slope)

NameError: name 'boot' is not defined

In the above example our estimated \(p\)-value is \(0\). As we only did \(1000\) samples this tells us our \(p\)-value is less than \(1/1000\).

18.12. Different Test Statistics for Hypothesis testing#

One might wonder why we used the slope of the line between \(X\) and \(Y\) as opposed to the correlation coefficient, \(r\), another measure of a relationship between \(X\) and \(Y\), or even \(R^2\). The truth is our choice here was arbitrary and if you prefer you can use these other options as our test statistic. However, these are all related by the following formulas,

This means if you run a permutation test it shouldn’t make a difference which test-statistic you use the p-values should all be the same!

18.13. Bootstrap Confidence Intervals for Regression#

Since our diabetes data set appears to satisfy the assumptions of linearity and heteroscedasticity we can proceed with building a basic bootstrap confidence interval for the slope of our regression line. Recall, the goal of the bootstrap confidence interval to build a confidence interval that contains the slope of the population regression.

The code below simulates \(1000\) samples of the original data set. We then compute the slope of the regression line, and store the difference between that and our sample slope in the bootstrap. Then use quantiles to compute the bounds of the interval.

np.random.seed(118)

sample_slope = ols(diabetes["BMI"],diabetes["BP"])[0]

boot_dist=[]

for i in range(1000):

# single bootstrap resample

boot = diabetes.sample(len(diabetes),replace=True)

# compute bootstrap statistic

boot_slope = ols(boot["BMI"],boot["BP"])[0]

#store bootstrap statistic - sample statistic

boot_dist.append(boot_slope-sample_slope)

# compute bounds for bootstrap distribution at 95% level

L0 = np.quantile(boot_dist,0.025)

U0 = np.quantile(boot_dist,0.975)

# print basic bootstrap interval

print("CI for slope at 95% level is ", [sample_slope-U0,sample_slope-L0])

CI for slope at 95% level is [0.9463984113473562, 1.5183717810998987]

Bootstrap confidence intervals for the slope of the regression line is important because it’s a single number that gives a good overview of the relationship between two variables. For instance, we can interpret the above as stating that for an increase of BMI of \(1\), that there’s an increase in Blood Pressure of between \(0.95\) and \(1.52\).

18.14. Bootstrap Confidence intervals for the Conditional Mean#

Confidence intervals for the slope are interesting because the slope provides a great summary for the relationship between two variables. However, we might frequently be interested in predicting the mean of \(Y\) for given \(X\) values. That is we want to find confidence intervals for \(\mu_{Y\mid X}\).

Let’s say we want to predict the average Blood Pressure of a diabetes patient with a BMI of \(30\). Here we use the percentile method.

boot_dist =[]

np.random.seed(121)

for i in range(1000):

# single bootstrap resample

boot = diabetes.sample(len(diabetes),replace=True)

# compute bootstrap statistic

boot_line = ols(boot["BMI"],boot["BP"])

#store output of regression line.

boot_dist.append(boot_line[0]*30+boot_line[1])

l0 = np.percentile(boot_dist,2.5)

u0 = np.percentile(boot_dist,97.5)

print("95% CI for average BP with BMI of 30 is ",l0,u0)

95% CI for average BP with BMI of 30 is 97.45479859582112 100.79594533746324

Frequently we might want to graph the CI for \(\mu_{Y\mid X}\) as \(X\) changes. To do this efficiently this we will bootstrap a bunch of regression lines, then to find the confidence intervals we’ll evaluate them and then find the percentiles.

boot_lines =[]

np.random.seed(121)

for i in range(1000):

# single bootstrap resample

boot = diabetes.sample(len(diabetes),replace=True)

# compute bootstrap statistic

boot_line = ols(boot["BMI"],boot["BP"])

#store the regression line

boot_lines.append(boot_line)

boot_lines = np.array(boot_lines)

#evaluate all of the lines

#To evaluate these lines efficiently, we can use multidimensional array slices

#This line evaluates all of the lines at a bmi of 30.

boot_dist = boot_lines[:,0]*30+boot_lines[:,1]

l0 = np.percentile(boot_dist,2.5)

u0 = np.percentile(boot_dist,97.5)

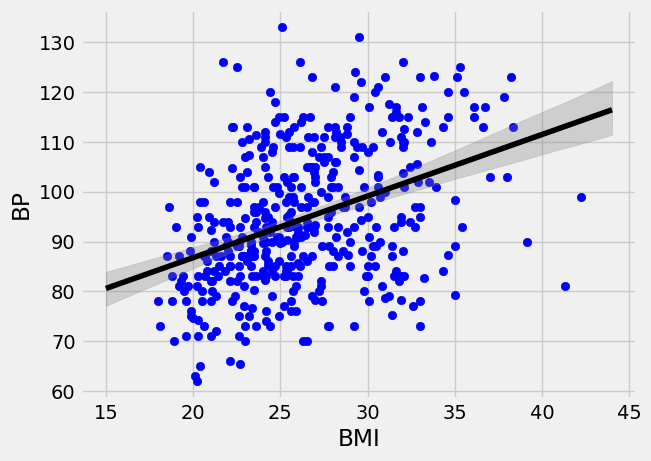

To graph this effectively we can then use the matplotlib method fillbetween.

plt.scatter(diabetes["BMI"],diabetes["BP"],color="blue")

plt.plot(np.arange(15,45), lin_regress[0]*np.arange(15,45)+lin_regress[1], "-",color="black");

# compute upper and lower bounds for the conditional mean mu_{Y|X}

yl0 = []

yu0 = []

x_val = np.arange(15,45)

for x in x_val:

dist = boot_lines[:,0]*x+boot_lines[:,1]

yl0.append(np.percentile(dist,2.5))

yu0.append(np.percentile(dist,97.5))

#Shaed in the region between the yl0 and yu0, with a grey color and opacity of 0.3

plt.fill_between(x_val,yl0,yu0,color="grey",alpha=0.3);

plt.xlabel("BMI")

plt.ylabel("BP")

plt.show()